Debt-Free Living for Photographers

December 9, 2020

I’ll be the first to admit that I hate finances. Budgeting is THE WORST. Math and numbers make me cringe. But the truth is, those things are the very reason I am where I am today. Married, living in my own home with three kids, paying for private health insurance, contributing to two IRA accounts for my husband and myself and contributing to three different College Savings 529 accounts for my children. Debt-Free Living.

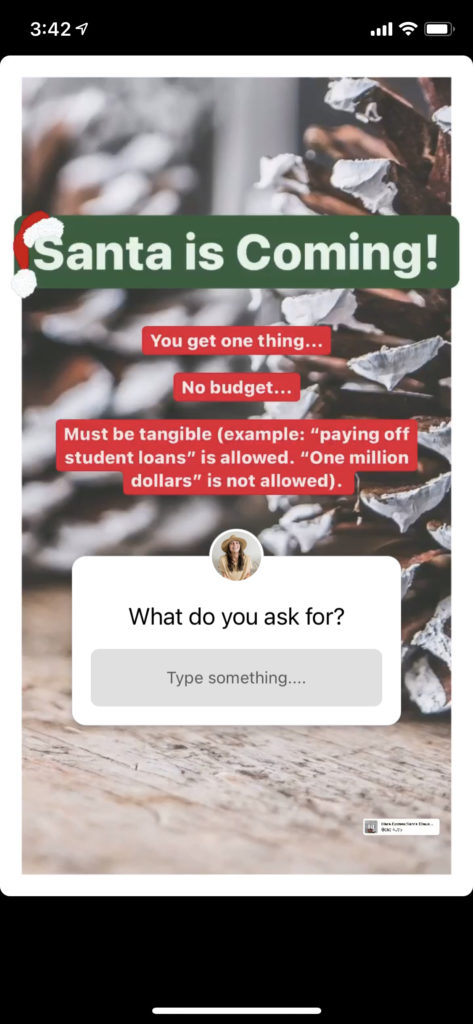

You might be wondering why I’m talking to you about finances, isn’t marketing my thing? Yes, it is! But the other day I was playing a fun game with my followers on Instagram Stories. Here is what I posted:

I was a bit surprised to see how many answers had to do with finances. Student loans, mortgages and debt were all a common theme amongst the dozens of responses I received.

I’ve always known debt was prevalent but after seeing your answers, I did a quick google search to try and truly grasp the national debt crises. Needless to say, I got lost in a sea of articles explaining just how bad it actually is.

Some of the most shocking statistics were:

- As of October 2019, “The national total student debt is now over $1.5 trillion.” (Citation)

- “More than 3 million senior citizens in the US are still paying off their student loans.” (Citation)

- “63% said they would give up paid time off in exchange for help paying off student loan debt.” (Citation)

I posted each of the responses (anonymously) and revealed some of the stats above. In one of the responses I mentioned that my husband and I attempt debt-free living and asked if you guys wanted a blog post on how. You said yes! So here it is!

6 money mindsets to achieve debt-free living

Money Mindset #1- debt won’t get you ahead

Student loan debt is part of a larger problem that has been woven into our society. The belief that debt is a normal part of life. But the truth is, it’s not. Debt negatively effects not just the economy but real people. You may be one of the millions who are overwhelmed by student loan debt. DEBT IS NEVER WORTH IT.

A lot of people go into debt because they think it’ll get them ahead. It doesn’t. Debt actually keeps you behind. I don’t care if it’s $50,000 in student loans or $500 for that lens you really wanted. IT WILL NOT GET YOU WHERE YOU WANT TO GO.

Did you know that I built my six-figure biz with two lenses? Two. Gear is important but it’s not everything. Even when I have had more than enough money to buy more gear, I don’t. I can never justify it in my mind. I also don’t spend a dime on marketing. Click HERE for 10 free ways to market your business!

Going into debt is like agreeing to walk around life with a 400 pound weight hanging over your head. Debt creates enough risk to counter any possible advantage. You deserve better. Future you deserves better.

Money Mindset #2- Sacrifices are required

Debt-free living requires you to realize one thing, you will make sacrifices! Your new rule is this: if you don’t have the money to pay for it, you have no business getting it. If you want to buy a new lens, you must make sacrifices. You must either increase your income or move money from one portion of your budget to another. Want to renovate your kitchen? You need to give up things in your lifestyle NOW so you can live better later.

If you have accumulated debt in your marriage, I encourage you to use Dave Ramsey’s Baby Steps as guidelines for paying off debt and building wealth simultaneously.

Money Mindset #3- Money doesn’t equal worth

The reality is, most people around us have accumulated debt. So when you start to freak out that you don’t have enough bookings for next year and are about to drop a bunch of money on ads or that one photographer on Insta’s 70-200 lens, remember this. Statistically, they are more than likely living a burdensome existence with payments out the wazoo on top of what is most likely student loans living in their attic. They might look like the have it all together but in reality, their world might be the most broken. Instead, fill your life with debt-free living role models who will remind you of what truly matters.

If you find yourself falling in the comparison trap, I recommend Rachel Cruze’s book, Love your Life, Not theirs. She will teach you how to quit playing the comparison game, think before you spend money, and start saving like you mean it. (CLICK HERE)

MONEY MINDSET #4- It won’t buy happiness

We’ve all heard the saying that “money doesn’t buy happiness.” But it’s actually true. I have found that people who try to buy more and more stuff are just covering up feelings of powerlessness and low self-confidence. But any confidence boost or power that you might get from buying more stuff isn’t real.

Buying an 85mm isn’t really going to help you overcome that nagging sense of self-doubt and insecurity. Spending $200 on ads most likely won’t bring you consistent and loyal business.

Money Mindset #5- It isn’t hopeless

It’s a scientific fact that when human beings feel overwhelmed, they begin to feel hopeless. And when we feel hopeless we become paralyzed and don’t accomplish goals (or even to-do lists). Our mental health goes awry and then everything just spirals.

Maybe you thought this was just you, but it’s not. When stressful things happen, things like:

- financial distress

- significant life changes (moving, divorce, giving birth, etc.)

- Death of a loved one

- Personal trauma

- Lack of Sleep

- Mental Health Illnesses

- Demanding Jobs

- Bad Nutrition

it triggers a physiological response in our body that releases cortisol, “the stress hormone.” It surges through our body leaving us with intense feelings of anxiety. At the very same time that is happening, serotonin, “the happy hormone” that helps us ward off depression/anxiety begins to deplete. This leaves us with feelings of despair and hopelessness.

If I can get a vulnerable for a second, this happened to me in the year 2020. Not only did I suffer a concussion that left me feeling unlike myself and unable to think and piece words together like I once could (which was killer since I’m in large part an enneagram 5) but then COVID on top of all of that.

I live in Illinois. Our state was shut down. I’ve lost over $60,000 in cancelled or postponed weddings and as it is, i’m not getting very many 2021 inquiries because Illinois brides are to fearful to have their weddings in 2021. For all of 2020 we haven’t been able to have gatherings over 50 people and according to our governor, until a vaccine is readily available to all the public, it won’t go back to normal.

Not only is that a tremendous amount of job stress on me but as the ONLY breadwinner for my family of 5, who has to pay private insurance and all the things, my anxiety this year has been through the roof. I’ve dealt with a lot of hopeless feelings.

But if I may say, no matter how hopeless we may feel there IS a light at the end of the tunnel! Keep fighting. But how?

- First, cry. Let it all out and don’t hold back. Write out all your angry feelings and sad feelings. All your fears.

- Then you’re going to sit down and make a plan. So that you realize these things that must get done (like debt-free living) aren’t actually mountains but molehills. Here’s how:

- List all of your debts from smallest to largest (ignore interest rate)

- Keep paying all the minimum payments like normal. But, the lowest debt will get attacked with everything you’ve got. Any extra income you get will go towards paying it off. Keep it going until every single debt on your list is gone.

If you need some help, I highly recommend taking a class like Financial Peace University and listening to Dave Ramsey’s podcast: The Dave Ramsey Show all the time. Listeners are constantly on there telling their stories of how they’ve achieved their debt-free living victories. These are super encouraging and will inspire you to keep going on really hard days.

Money Mindset #6- Know your limits

Time and Money are both commodities. And if you don’t tell them where to go, you’ll wonder where they went. I talk about productivity tips in THIS BLOG post. But I want to talk about budgeting here.

Budgeting doesn’t mean tracking your expenses after they happen. Budgeting is preparing ahead of time and setting aside money for upcoming expenses. When my hubby and I do this, we assign a name to EVERY SINGLE DOLLAR we will be making.

Here is how we make our budget:

- Identify your Income. A lot of photographers mix their business and personal dollars. I recommend keeping them separate. Not only does this help at tax time at the end of the year but it also helps in times of national crises like this year. Because I pay myself a regular paycheck amount every single Friday I was able to get a forgiveable PPP loan from our government, something a lot of creatives weren’t able to snag. So make sure you set up TWO different accounts. One for your biz and one for your family.

- After identifying your income, write down your fixed expenses. Things like: mortgage, health insurance, car insurance, car payments, home owners insurance, life insurance, internet, etc. If your insurance premiums are due twice a year, just divide the cost throughout the months and then save steadily.

- Then, write down your common monthly expenses. Start with variable expenses like: water bill, gas, electricity, phone bill, etc. And then move on to more optional expenses like: netflix, disney+, eating out, fun money, clothing, memberships, etc.

- Now, we will consider monthly goals. Think about where you want to be financially next year. This is where you really work to create the life that you want tomorrow. Once you have the goals, you’ll need a plan to make them happen (see above). Then, add that plan to your budget.

- Use a zero-based budget (source). That doesn’t mean you will have $0 in your account but rather that every dollar has a job. You get a zero-based budget by putting in all your expenses until you reach zero: INCOME – EXPENSES = $0. If there is money left over after all your expenses, put it toward your money goal (whether thats paying off debt, buying a new lens, etc.)

For budgeting help I highly recommend checking out the budget app, EveryDollar. It makes creating a budget super easy and you can take it with you wherever you go. Literally cannot say enough good things about this app.

Bonus lesson’s we’ve learned when creating a budget…

- Keep a buffer in your bank account. Avoid overdraft fees and etc by having at least $50-$100 in your checking account at all times. Pretend it’s not there. To make sure it’s there, put it as an expense in your first month’s budget.

- Track your spending. This is why I love the app. Instead of tracking our spending at the end of the month, this app allows us to be attentive to our spending all month long so we can adjust as needed.

- Savings. Not every expense is able to be planned. For example, my hubby and I knew my car battery was getting worse so we began to save for a new one. When it finally went out, it was no big deal.

- Emergency Fund. This is one of Dave Ramsey’s 7 baby steps that I linked to above, but it’s important enough to mention just in case! My hubby and I have a separate savings account for our family and then I have one for my business. In it, we keep 3-6 months of our living expenses at all times. So for my business, I keep 3-6 months worth of paychecks in it. For our family, we keep 3-6 months of our costs of living in it. That way when a true emergency happens you are always prepared. Definitely read the article though. He talks about how to do this that while paying off debt (source).

Don’t forget, Debt-Free living is possible! You are in control of your money… not the other way around!